3 min read

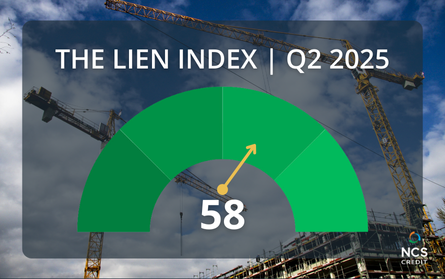

Lien Index down 2 points to 58 from revised Q1 score of 60.

The Lien Index ended Q2 2025 at 58; an approximate 3% decline in activity from Q1 2025.

National Mechanic’s Lien Activity

Overall, lien activity remains high as contractors and suppliers grapple with bankruptcies, cash flow issues, rising costs, and project delays, using liens strategically to secure payments and manage risks amid economic uncertainty.

Regional Mechanic’s Lien Activity

Lien activity in the South climbed 3% from 68* in Q1 to 70 in Q2. And, although activity declined in the Northeast (down 5% from 63* in Q1 to 60 in Q2), lien activity was well above average, signaling persistent payment issues. The West’s lien activity decreased 9% from 54* in Q1 to 49 in Q2 and the Midwest saw the steepest drop at 16% lower in Q2 (42) than Q1 (50*).

States with Highest Mechanic’s Lien Activity

The top 5 states for lien activity were (in order of volume): Texas, Florida, California, Nevada and new to the top five this quarter is Georgia.

Top 3 States by Region

- West: California, Nevada, Colorado

- Midwest: Ohio, Iowa, Illinois

- South: Texas, Florida, Georgia

- Northeast: New York, Massachusetts, New Jersey

Looking Forward

The construction industry continues to face significant headwinds that strain both operations and finances. Labor shortages remain one of the biggest challenges, causing project delays, driving up costs, and making it difficult for contractors to keep projects on schedule. Even as material availability improves in some sectors, finding skilled workers remains a persistent obstacle, slowing productivity and increasing the cost of completing projects.

Compounding these pressures are rising borrowing costs, which squeeze cash flow for businesses already operating on thin margins. Price volatility for materials and equipment, project delays, and cost overruns are creating uncertainty and fueling more frequent disputes over contracts, change orders, and payment terms. Not to mention bankruptcies are adding risk, as suppliers and contractors face growing concerns about getting paid for completed work or delivered materials.

Extended credit terms, once a competitive necessity, are becoming increasingly risky, leaving suppliers and subcontractors vulnerable if payments stall. Meanwhile, shifting dynamics in commercial real estate, particularly in office and retail sectors, are influencing project funding and market confidence. While lien filings dipped slightly in Q2, the data reflects an industry operating cautiously, balancing the pursuit of new opportunities with the need to protect cash flow and manage growing financial risks.

We cannot stress this enough: serve preliminary notices and secure mechanic’s liens and bond claims on every construction project, and file UCCs on any customer with an open line of credit. While you can’t control the economic landscape, you can control how well you prepare for it. Taking these proactive steps is essential to protecting your business and ensuring you get paid, no matter what challenges arise.

Industry Experts

The AIA/Deltek Architecture Billings Index (ABI) ended Q2 at 46.8, with firms reporting a decrease in billing. “Inquiries into new projects increased for the second consecutive month and grew at the strongest pace since last fall with a score of 53.6, indicating clients are starting to send out RFPs and initiate conversations with architecture firms about potential projects after a lull since mid-winter. These inquiries do not necessarily translate into actual projects, as the value of newly signed design contracts declined for the 16th consecutive month in June. It is unlikely that firm billings will return to positive territory until the value of new design contracts also starts to increase again.” – AIA/Deltek Architecture Billings Index June Report

Associated Builders and Contractors (ABC) reported its Backlog Indicator rebounded by the end of Q2. “Despite a wide array of headwinds and disappointing construction spending data in recent months, backlog rebounded to 8.7 months in June, the same level as in April,” said ABC Chief Economist Anirban Basu. “In addition to longer backlog, contractors remain broadly optimistic, with 3 in 5 contractors expecting their sales to rise during the second half of 2025,” said Basu. “Notably, this survey predates the most recent trade policy announcements, and 1 in 5 contractors had a project interrupted or paused due to tariffs in June. With some of the newest import taxes putting upward pressure on construction input prices, profit margin expectations may face pressure in the months to come.”

The Dodge Momentum Index grew throughout Q2. “Nonresidential planning steadily improved in June, alongside strength in warehouse, recreational, and data center planning,” stated Sarah Martin, Associate Director of Forecasting at Dodge Construction Network. “Planning momentum in other key sectors – like education, hotels, and retail stores – was more subdued. Expectations for weaker consumer spending and travel demand, as well as volatility around funding, are likely contributing to the weaker momentum of projects entering the planning queue for those sectors.”

Epiq Bankruptcy reported total bankruptcy filings increased 10% in the first half of 2025. “Elevated prices, increased borrowing costs and uncertain geopolitical events continue to add to the growing debt loads shouldered by financially distressed families and small businesses,” said ABI Executive Director Amy Quackenboss. *Nationwide, recording offices manage a backlog of requests. The Index data is adjusted and revised accordingly.

*Nationwide, recording offices manage a backlog of requests. The Index data is adjusted and revised accordingly.

Do Mechanic’s Liens Expire? What Happens After

Understand the importance of enforcing your mechanic's lien claim. Learn about deadlines, suit processes, and how to protect your rights effectively.

Lien Index Q2 2026

Explore the latest Lien Index findings for Q2 2026, revealing trends in mechanic's lien activity and insights into construction industry credit risks.

Healthcare Bankruptcies Are Rising: A Risk to Suppliers

Healthcare bankruptcies are up 300%+ since 2010. See what unsecured creditors really recover — and how a UCC filing changes the outcome. Free download.