3 min read

.png)

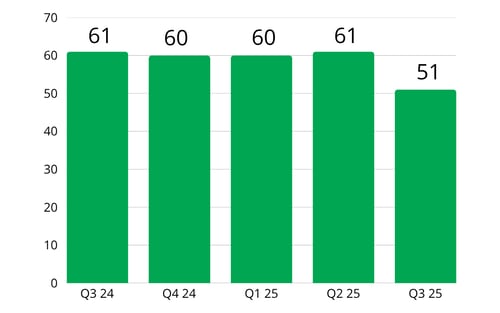

Lien Index Falls 10 Points (16%) to 51 from Revised Q2 Score of 61, Signaling Shifts in Market Activity

NCS Credit's Lien Index is derived from carefully monitored national and regional mechanic’s lien activity, construction economic data from various sources, and general economic trends. The Lien Index compares mechanic’s lien data, quarter over quarter. The standard is fifty (“50”), with a number greater than "50" representing an increase in mechanic’s lien activity, and less than "50" representing a decrease in mechanic’s lien activity.

National Mechanic’s Lien Activity

The Lien Index dropped to 51 in Q3 2025 after holding in the 60s for more than a year, marking a notable shift in lien activity. Fewer filings could indicate improved payment behavior in some segments but may also reflect slower project starts and reduced activity as contractors navigate ongoing economic and labor challenges. The data points to a market adjusting to new economic realities and shifting construction demand.

Regional Mechanic’s Lien Activity

Regional Mechanic’s Lien Activity

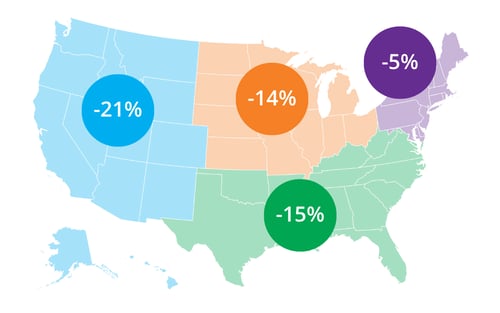

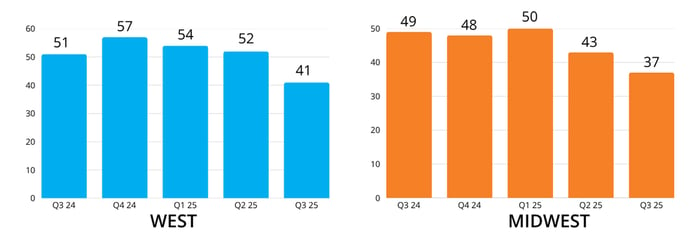

Lien activity declined across all regions in Q3, signaling a broad cooldown in mechanic’s lien filings. The West saw the largest decrease, down 21% from 52 in Q2 to 41, slipping below the baseline of 50.

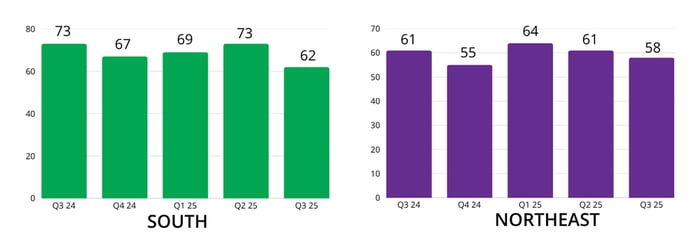

The Midwest followed with a 14% decline, falling from 43 to 37, while the South dropped 15% from 73 to 62 after leading the nation in filings last quarter.

The Northeast experienced a smaller decline, down 5% from 61 to 58, but remained above the 50 threshold, indicating continued elevated activity in the region.

States with Highest Mechanic’s Lien Activity

The top 5 states for lien activity were (in order of volume): Texas, Florida, California, Georgia and Nevada.

The top 5 states for lien activity were (in order of volume): Texas, Florida, California, Georgia and Nevada.

Top 3 States by Region

- West: California, Nevada, Colorado

- Midwest: Iowa, Ohio, Illinois

- South: Texas, Florida, Georgia

- Northeast: New York, Massachusetts, Pennsylvania

Looking Forward

The construction industry continues to face economic headwinds as costs rise and demand softens across key sectors. Total construction spending declined 2.8% year over year as of July 2025, one of the slowest growth periods in recent years (U.S. Census Bureau). Nonresidential activity, including commercial and manufacturing projects, has cooled, while public works and data center construction remain among the few areas showing steady growth (ABC.org).

Material costs and tariffs continue to disrupt budgets and delay projects. Steel, aluminum, and other imported building materials remain volatile, forcing contractors to reprice bids and postpone starts. Nearly one in four contractors report that tariffs have directly led to project delays or cancellations (ABC.org; S&P Global). Labor shortages further limit productivity, with skilled workers difficult to find and competition driving wages higher. Combined with rising borrowing costs and price fluctuations, these pressures are reducing margins and increasing disputes over contracts, change orders, and payment terms.

The Bottom Line: The industry is operating cautiously, balancing opportunity with growing financial risk. Rising costs, labor shortages, and market uncertainty make strong credit management essential. Serve notices, secure mechanic’s liens and bond claims, and file UCCs on all open accounts. While broader economic forces are outside your control, proactive measures ensure your right to payment is protected.

Industry Experts

The Architecture Billings Index (ABI) ended Q3 with its lowest reading (43.3) since April. “…[I]nquiries into new projects remained flat for the second consecutive month, following growth over the summer, and the value of newly signed design contracts decreased for the 19th consecutive month. All of these indicators mean that the soft conditions that many architecture firms have been experiencing since late 2022 are likely to persist for the foreseeable future.”

Associated Builders and Contractors (ABC) reported its Backlog Indicator dipped. “The dip in backlog observed in August is not surprising given ongoing declines in nonresidential construction spending,” said ABC Chief Economist Anirban Basu. “While backlog in the heavy industry and infrastructure categories has held up well, commercial and institutional backlog has not. With private sector projects struggling under the weight of rising materials costs, policy uncertainty and reemerging labor shortages, that category may remain weak over the next few quarters.

From the Dodge Momentum Index: Year-to-date, the DMI is up 33% from the average reading over the same period in 2024. “Planning momentum remained steadfast for data centers, healthcare, and public buildings throughout September and will correlate to stronger construction spending in early 2027,” stated Sarah Martin, Associate Director of Forecasting at Dodge Construction Network. “After a prolonged period of uncertainty, owners and developers are advancing projects into planning, but activity is expected to normalize in future months.”

Epiq Bankruptcy reported “As anticipated, bankruptcy filing volumes continue to climb, even as GDP shows growth and unemployment remains relatively stable,” said Michael Hunter, vice president of Epiq AACER. “Notably, we are witnessing the longest sustained increase in total open case inventory since 2008—a clear indicator of shifting financial pressures. Looking ahead, we expect this upward trend to persist into 2026, as bankruptcy protection filings return to pre-pandemic levels. Key factors contributing to future uncertainty include the impact of tariffs, the resumption of student loan obligations, and interest rates.”

Lien Index Q2 2026

Explore the latest Lien Index findings for Q2 2026, revealing trends in mechanic's lien activity and insights into construction industry credit risks.

Healthcare Bankruptcies Are Rising: A Risk to Suppliers

Healthcare bankruptcies are up 300%+ since 2010. See what unsecured creditors really recover — and how a UCC filing changes the outcome. Free download.

Full vs. Unpaid Balance Lien States Explained

Learn how full price and unpaid balance lien states affect your mechanic's lien rights as a subcontractor or supplier - and how to protect them.