Blog

Purchase Money Security Interest and Super-Priority

Secure your payments with Purchase Money Security Interest filings and super-priority status. Learn how to protect your assets and get paid.

Blog

Business Bankruptcies Are Rising; Time to Protect Your A/R

Commercial bankruptcies are rising across industries. Learn how UCC filings and mechanic’s liens can help you recover payment.

Blog

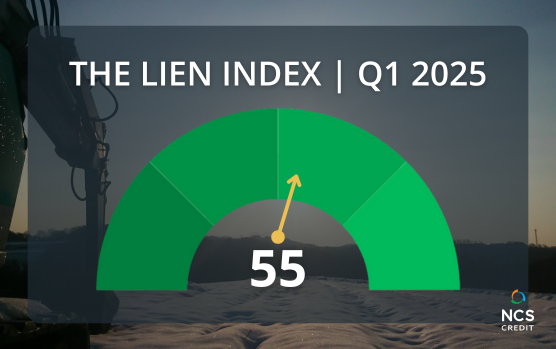

Lien Index Q1 2025

Lien Index down 5 points from Q4 to 55. Mechanic’s Lien activity has declined, but forecasted to increase in coming quarters.

Blog

UCC Filing Myths

Dispel the myths surrounding UCC Financing Statements and how they can benefit your credit process. Expert insights from NCS Credit.

Blog

Construction Litigation Attorney

Selecting the right attorney for construction litigations can impact your ability to secure receivables. Learn how to weigh your options.

Blog

Payment Protection Rights for Los Angeles Wildfires

Importance of protecting payment rights for material suppliers & subcontractors in the aftermath of the Los Angeles fires.

Blog

Reduce the Need for Collections with UCC Filings

Learn how UCC filings can reduce collections, secure your accounts receivable, and enhance your financial position as a creditor.

Blog

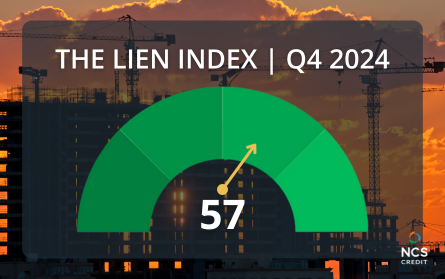

Lien Index Q4 2024

Slow payments continue to plague the industry, as the Lien Index Q4 2024 declined to 57, a 4 point drop from Q3 2024.

Blog

Preliminary Notices 101: A Beginner’s Guide

New to mechanic's lien and bond claim rights? Here's the top info you should know about preliminary notices.

Blog

Navigating Credit Trends in 2025

Credit will be shaped by tech innovations, regulatory changes, & evolving economic policies. Learn more about navigating credit trends in 2025.

Blog

Past-Due Accounts: Collection Agencies vs. Write-Offs

NCS Attorney, Michelle Gerred discusses why you should use a contingent collection service before writing off bad debt.

Blog

How to Spot and Avoid a Common UCC Filing Scam

Filing UCCs is one of the most common trade credit practices! Unfortunately, there are scammers that aim to take advantage. Learn how to spot a scam.