Everything You Need to Know about Washington Mechanics Lien and Bond Claim Rights

Starbucks, Jimi Hendrix, Bing Crosby, Mt. Rainier, Boeing and Microsoft come from the great state of Washington, the only state named after a president. The intense clean-up efforts of the Hanford Nuclear Waste site, the replacement of the Alaskan Way Viaduct, the continued expansion of the Sound Transit and the ongoing construction of mixed-use property (commercial & residential) in high population areas are driving construction in Washington.

In fact, according to ENRNorthwest, Seattle ranked at the top of U.S. cities with active construction cranes in 2018 (neighboring Portland, Oregon held its own in fourth place) much in part to the boom in mixed-use real estate construction.

Construction is awesome!

It is great for the economy, state infrastructure and, with a growing population, it’s a necessity. Unfortunately, construction projects also come with financial risks. 2018 was a big year for construction in Washington and predictions for 2019 are just as strong. Are you prepared to secure your Washington mechanic’s lien, stop notice, bond claim and public improvement lien rights?

Washington Mechanic’s Lien

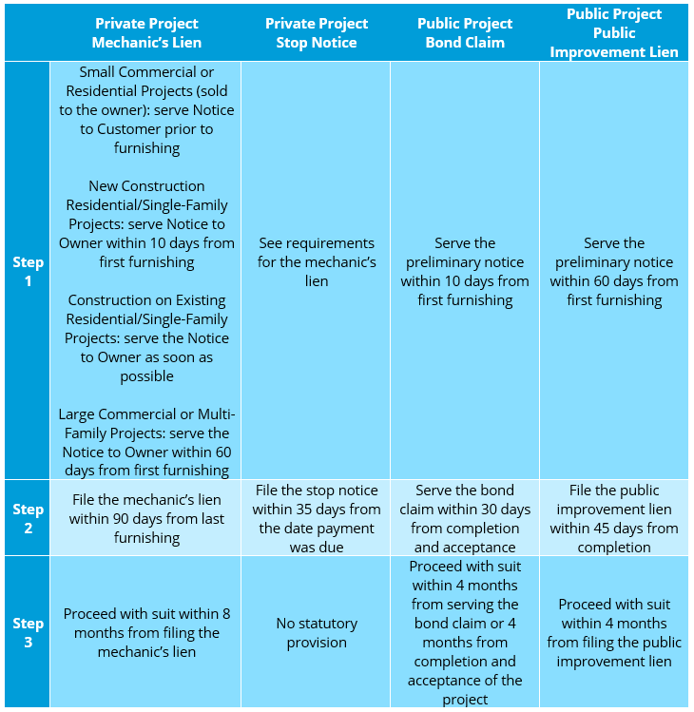

First Step? Timely Serve the Preliminary Notice!

Washington preliminary notice requirements are a bit intense, depending on the project type:

- On small commercial (when general contract is $1,000.00 or more, but less than $60,000.00; or 4 or fewer unit Residential Projects when general contract is more than $1,000.00), contractors who contract directly with the owner must serve a Notice to Customer upon the owner and obtain a signed copy prior to first furnishing materials or services. Contractor must retain the signed copy for three years.

- On commercial, multi-family, or small commercial projects, serve the Notice to Owner upon the owner and prime contractor within 60 days from first furnishing materials or services. A late notice may be served, but the lien, when later filed, will only be effective for materials and services provided 60 days prior to serving the notice and thereafter. The Notice to Owner is not required for subcontractors contracting directly with the prime contractor, laborers, and those contracting directly with the owner.

- On new construction of residential single-family projects, serve Notice to Owner upon the owner and prime contractor within 10 days from first furnishing materials or services. A late notice may be served, but the lien, when later filed, will only be effective for materials and services provided 10 days prior to serving the notice and thereafter. The Notice to Owner is not required for subcontractors contracting directly with the prime contractor, laborers, and those contracting directly with the owner.

- On construction of existing residential single-family projects, serve Notice to Owner upon the owner as early as possible. The lien, when later filed, will only be effective for amounts not yet paid to the prime contractor at the time the notice is received. The Notice to Owner is not required when contracting directly with the owner.

Second Step? Mechanic’s Lien Time!

Whether the project is commercial, residential, new or improvement, the mechanic’s lien deadline is the same: file the mechanic’s lien within 90 days from last furnishing and serve a copy of the lien upon the owner within 14 days from the filing of the mechanic’s lien.

OH! I nearly forgot, for commercial projects Washington is a full balance lien state. This means, the lien is enforceable for the full amount owed, regardless of payments made by the owner.

And one more tidbit: mechanic’s liens can be bonded off in Washington! But don’t fret – that just means your security changes from the property to the bond.

Third Step? Suit Up!

If the filing of a mechanic’s lien does not prompt payment, you should file suit to enforce the mechanic’s lien within 8 months from the filing of the lien.

Washington Stop Notice

First step? Timely Serve the Preliminary Notice!

Fortunately for you, me & this blog post, I don’t have to restate the information for serving a preliminary notice to secure stop notice rights. In fact, it is recommended you serve the preliminary notice as outlined for the mechanic’s lien section. This means I can literally say, see above! <<insert grin>>

Important Note: in Washington, a stop notice is not applicable if there is a payment bond of at least 50% of the amount of construction financing.

Second Step? Stop Notice Time!

Serve the Stop Notice upon the lender, owner and prime contractor after 5 days from the date payment was due, but within 35 days from the date payment was due. If the lender does not withhold the amount claimed from subsequent draws, the mortgage, deed of trust, or other encumbrance securing the lender shall be subordinated to your lien to the extent of the construction financing wrongfully disbursed.

Third Step? Suit Up!

Actually, statute does not include a provision for suit against the stop notice. In the event the lender does not withhold said payment, you may need to proceed with suit (think “breach of contract” type suit). Although I find statute fascinating, I am not an attorney & I strongly encourage you to seek legal guidance!

Washington Bond Claim

If you are furnishing to a public project in Washington you should always attempt to obtain a copy of the payment bond from the public entity which contracted the project. For that matter, any time you are furnishing to any public project across the US and even in Canada, always attempt to obtain a copy of the payment bond!

Generally, payment bonds are required on all public work contracts. General contracts of $150,000.00 or less may be exempted from the bonding requirement provided 10% of the contract amount is retained by the owner for a period of 30 days after final acceptance.

First Step? Timely Serve the Preliminary Notice!

Serve notice upon the prime contractor within 10 days from first furnishing. The notice is not required when contracting directly with the prime contractor or when providing only labor.

Pro Tip: a notice may not be required, but as a best practice, you should ALWAYS serve a preliminary notice

Second Step? Bond Claim Baby!

Serve and file the bond claim notice with the public entity within 30 days from completion and acceptance of the project.

Third Step? Suit Up!

File suit to enforce the bond claim in accordance with the terms and conditions of the payment bond. It is recommended that suit be filed to enforce the bond claim after 30 days from filing the bond claim, but within 4 months from filing the bond claim or 4 months from completion and acceptance of the project.

Washington Public Improvement Lien

First Step? Timely Serve the Preliminary Notice!

Material suppliers must serve notice upon the prime contractor within 60 days from first furnishing materials or services. A late notice may be served, but the lien, when later filed, will only be effective for materials and services provided 60 days prior to serving the notice and thereafter. No notice is required when contracting directly with the prime contractor or when providing only labor.

Second Step? Public Improvement Lien Time!

Serve and file the lien upon the public entity within 45 days from completion of the project. The claim is a lien on the funds the public entity is required to withhold from the prime contractor. Serve and file the lien as soon as possible to trap the funds.

Third Step? Suit Up!

If serving the public improvement lien does not prompt payment, you should file suit to enforce the public improvement lien within 4 months from the filing of the lien.

Side by Side Comparison

There is a LOT of information in this post, so I thought a table may help!

Questions about lien and claim rights in Washington? Contact us today!