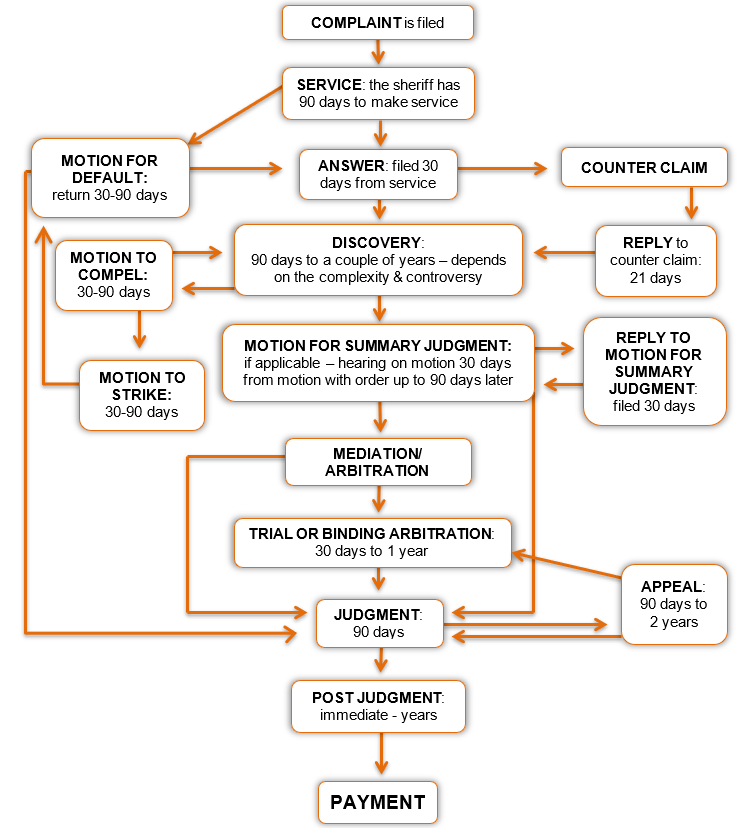

Progress Payments Have Stopped, Now What Should You Do?

Progress payments are payments made as work progresses under a contract, upon the basis of costs incurred, percentage of completion accomplished, or a specific stage of completion. Progress payments may be made from the owner to the general contractor, the general contractor to its subcontractors/suppliers, the subcontractor to its suppliers, etc.

Progress payments have positive potential, as they can eliminate the need for various parties to finance a project. Unfortunately, if the progress payments stop, progress on the project may stop.

No Payment, Now What?

Julie Weller of Faegre Baker Daniels advises a contractor has two choices when an owner stops making payments: “It can either continue to perform the work or cease the work…” As you’d imagine, neither of these options is appealing for a multitude of reasons.

Weller’s article, Progress Payments: What to Do When the Money Stops Trickling In, focuses on the owner/general contractor dynamic. Ordinarily, NCS would recommend moving forward with a mechanic’s lien or bond claim, but Weller recommends carefully reviewing the contract and determining whether payment is “clearly due and owing.”

What’s in the Contract?

Contract terms can be tricky. Hidden among long legal sentences and paragraphs of tiny font you may find provisions regarding payment, suspension and termination.

Weller recommends carefully reviewing these provisions, as they may include notice requirements, and if ignored, the general contractor could be in breach of its contract.

“If the contract expressly states that the contractor must give notice of intention to stop work, the contractor must do so or it will be in breach of contract. Many contracts require the contractor to continue performance despite any ongoing dispute, even those that relate to payment. The contractor should consider the consequences if it does not make payment to its subcontractors – its failure to pay its subcontractors, despite not being paid by the owner, could be a breach of its contract with the owner and its contract with the subcontractors.”

Many of our clients, typically subcontractors and suppliers, come to us with the same story, “The GC says the owner isn’t paying him, so he can’t pay us.” This inevitably leads to the review of contracts for contingent payment clauses, and to mechanic’s lien filings or enforcement of arbitration clauses. If I could plead a case to general contractors, I would beg you to continue paying parties you have hired!

Next Up: “Clearly Due & Owing”

Yikes, very few things are “clear” in construction, unless we consider mud to be clear. In her article, Weller states that an owner will not be held in breach of contract if the payment is not “clearly due and owing.” Further, in the long run on sentences & tiny font of the contract, there may be provisions allowing the owner to withhold money.

Weller provides the following situations which may permit the owner to withhold payment:

- Defective work not remedied

- Claims filed by a third-party

- Failure of the contractor to pay its subcontractors

- Reasonable evidence that the work cannot be completed for the remainder of the contract sum

- Damage to the owner or another contractor

- Reasonable evidence that the work will not be completed within the contract time, and the unpaid balance is not enough to cover damages for the anticipated delay

- Persistent failure to carry out the work in accordance with the contract

It’s worth noting, the owner should only withhold the amount that corresponds to the circumstance. This means, if the owner is withholding payment because the contractor hasn’t paid its subcontractor, the owner can only withhold the amount of the subcontractor’s claim. Another example is if the contractor has successfully completed the foundation, but has failed to complete the piping, the owner can only withhold money for the incomplete piping.