Understanding Texas Notice Cycles for Lien and Bond Rights

That’s an odd title, right? “Texas Preliminary Notices Are for Non-Payment.” It may sound odd, but for good reason. In most states, preliminary notices are proactive and the first step in the mechanic’s lien process, meaning you serve the notice before you begin furnishing or shortly after you start furnishing. But in Texas, the notice is reactive because you only serve the notice if you haven’t been paid, hence, the notices are for non-payment. It can be confusing, fortunately NCS Credit is here for you. In this post we’ll review the Texas notice cycle when you are furnishing to a commercial private project or public project.

Notice of Non-Payment vs. Notice of Claim for Unpaid Labor or Materials

The key difference between a Notice of Non-Payment and a Notice of Claim for Unpaid Labor or Materials is in timing and formality. Under the old statute, claimants had to send second- and third-month Notices of Non-Payment without a required format. As of January 1, 2022, Texas law replaced that with a single, standardized notice that must be sent by the 15th day of the third month after labor or materials are provided, using the format outlined in the statute.

*Note: although the term Notice of Non-Payment has been replaced for private projects, it still applies to public projects.

What Is a Notice of Claim for Unpaid Labor or Materials?

A Notice of Claim for Unpaid Labor or Materials (Texas Property Code Sec. 53.056) is a notice sent to preserve mechanic’s lien rights, and it advises payment is due or past due. Generally, the notice should be served upon all parties in the ladder of supply and sent via certified mail return receipt requested.

What Is a Notice of Non-Payment?

A Notice of Non-Payment was an informal term used in Texas to describe the preliminary notices that subcontractors and suppliers were required to send to preserve their mechanic’s lien rights under the prior version of the Texas Property Code. Much like the Notice of Claim for Unpaid Labor or Materials, these notices were served to alert the property owner and original contractor that payment had not been received.

What Is a Prelien Notice?

A prelien notice is a general term for a written notice sent by subcontractors, suppliers, or others who provide labor or materials on a construction project. Its purpose is to inform the property owner, general contractor, or lender of their involvement and protect their right to file a mechanic’s lien if unpaid. However, the exact name, timing, content, and recipients of such notices are dictated by state statutes, so “prelien notice” is a broad, non‑state‑specific term. Each state may have different required notices with specific legal names and formats.

Texas Mechanic’s Lien Statute Changes

The 2021 statute changes apply to any general contract executed on or after 01/01/2022 for private commercial or residential projects (no changes were made for public projects). Likely, your rights align with the revised statute. Now, let’s address a few items from the 2021 changes to Texas statute.

Under the 2021 statute changes, the Notice of Non-Payment became the Notice of Claim for Unpaid Labor or Materials. Additionally, the Notice of Retainage became the Notice of Claim for Retainage. And, for our Texas-notice-veterans, you no longer need to serve a 2nd month notice on private projects. (Wondering what changed? You can download a comparison of the 2021 changes.)

Pros and Cons of the 2nd Month Notice

For those Texas-notice-veterans who (like us) find the 2nd month notice beneficial, you can certainly continue sending them. In our experience, serving the 2nd month Notice of Non-Payment, which was required under the previous version of Texas’ statute, is an excellent opportunity to notify parties that you haven’t been paid. It’s also a best practice to serve the notice if you are unsure when the general contract was executed, to ensure your rights are protected: It’s better to serve an extra notice than miss the required notice.

Now, there is a caveat here. Depending on who you’ve contracted with and their knowledge of the statute, you may irritate a party by serving the 2nd month notice because it’s no longer required. So, as a business, you’ll want to weigh your options (i.e., is it better to try and prompt payment because you’ve already gone 60ish days unpaid OR is it better to preserve the relationship and not ruffle any feathers).

Ultimately, if you are unsure when the general contract was signed or if you’ve found the 2nd month notice beneficial in collecting payment, go ahead and send the notice!

When Should a Notice of Claim for Unpaid Labor or Materials be Served?

For private commercial projects, you should serve the notice no later than the 15th day of the third month following each month in which materials or services were furnished.

Texas Notice Deadlines Fall on the 15th

Here’s the best and worst thing about securing mechanic’s lien or bond claim rights in Texas: notices, mechanic’s liens and bond claims are all due by the 15th of the month. It’s awesome! You’ll never miss a deadline because it will always be the 15th of the month, except… Well, Texas deadlines are also based on months not paid, in a rolling month format.

Here’s an Example

Let’s say you furnished materials in April. If you aren’t paid for what you supplied in April, then you must send a Notice of Claim for Unpaid Labor or Materials by July 15th.

Schedule for Notice of Claim for Unpaid Labor or Materials

Example for one month of furnishing

| Month of Furnishing | Third Month Notice | Mechanic’s Lien* |

| January | April | May |

| February | May | June |

| March | June | July |

| April | July | August |

| May | August | September |

| June | September | October |

| July | October | November |

| August | November | December |

| September | December | January |

| October | January | February |

| November | February | March |

| December | March | April |

Seems simple enough, right? It is, until we start adding in other months of furnishing.

So, now let’s say you furnished in April and May. You’ll still serve a Notice of Claim for Unpaid Labor or Materials by July 15th if you aren’t paid for your April furnishing, but now you also need to keep tabs on your May furnishing.

If you aren’t paid for what you supplied in May, then you’ll serve a Notice of Claim for Unpaid Labor or Materials by August 15th.

Schedule for Notice of Claim for Unpaid Labor or Materials

Example of two months furnishing

| Month of Furnishing | Third Month Notice | Mechanic’s Lien* |

| January | April | May |

| February | May | June |

| March | June | July |

| April | July | August |

| May | August | September |

| June | September | October |

| July | October | November |

| August | November | December |

| September | December | January |

| October | January | February |

| November | February | March |

| December | March | April |

It’s critical for you to send these notices for each month that you furnish materials or labor for which you remain unpaid.

Wait, Does that Mean I Have to File Multiple Mechanic’s Liens?

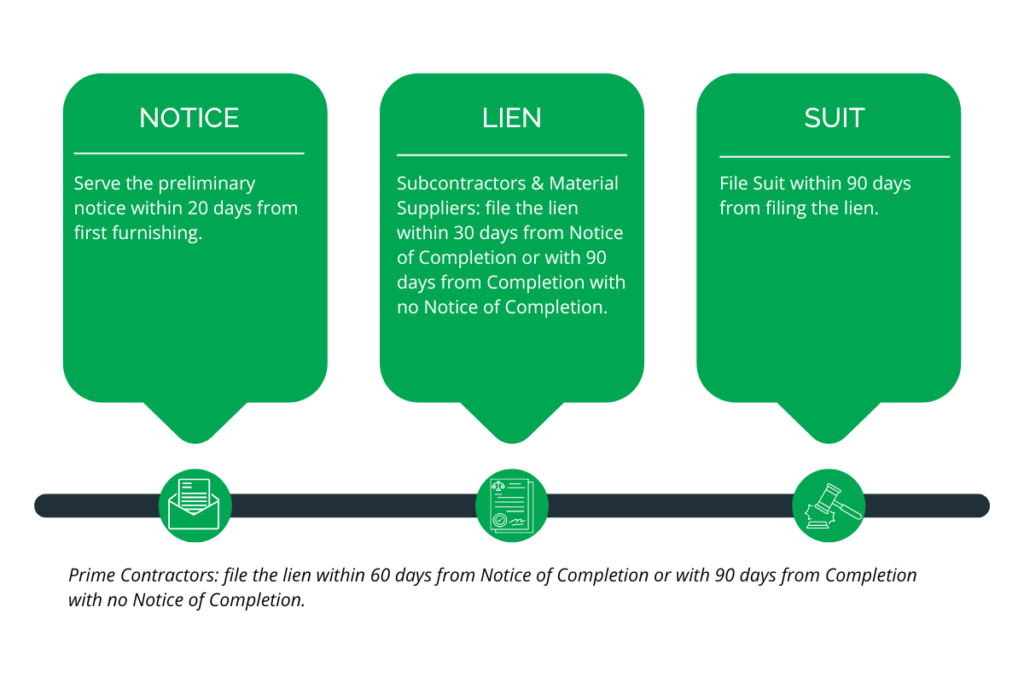

No, you do not need to file multiple mechanic’s liens. For commercial projects, your mechanic’s lien deadline will depend on whether you sold to the general contractor, subcontractor or material supplier.

- Selling to the general contractor, you will file your lien no later than the 15th day of the fourth month from completion, termination, or abandonment of your contract.

- Selling to a subcontractor or material supplier, you will file your lien no later than the 15th day of the fourth month after the last month you furnished.

So, if we go back to our earlier example (and we’re selling to a subcontractor or material supplier), our lien deadline based on April and May furnishings would be September 15th.

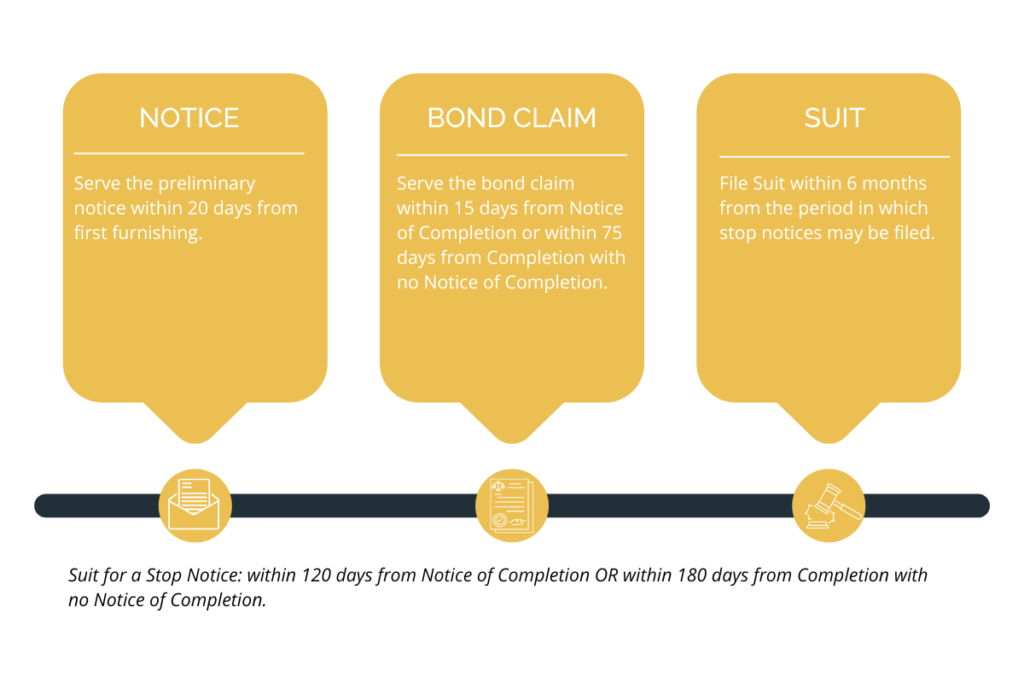

Serve a Notice of Non-Payment on Public Projects

Before we hit the high points, the notice served for public projects is called a Notice of Non-Payment (there weren’t any statute changes for public projects). Although the name (and text) is different, the overall concept is the same.

If you are selling to a subcontractor on a public project, you must serve a Notice of Non-Payment no later than the 15th day of the second month following each month in which materials or labor were furnished for which you remain unpaid. Then, serve the bond claim notice (aka Sworn Statement of Account in compliance with Texas Government Code Sec. 2253.041) no later than the 15th day of the third month following each month in which you furnished.

Let’s go back to the example from the private project above.

If you aren’t paid for your April furnishing, you must send the 2nd month Notice of Non-Payment by June 15th. Then, if July comes along, and you still haven’t been paid for the April furnishing, you must serve the bond claim (Sworn Statement of Account) by July 15th.

If you remain unpaid for May furnishings, a 2nd month notice will be due by July 15th, and a bond claim is due by August 15th.

Note: unlike mechanic’s liens, bond claims must be served for each month that you remain unpaid.

Schedule for Notice of Non-Payment

Example of two months furnishing

| Month of Furnishing | Second Month Notice | Bond Claim (Sworn Statement of Account) |

| January | April | May |

| February | May | June |

| March | June | July |

| April | July | August |

| May | August | September |

| June | September | October |

| July | October | November |

| August | November | December |

| September | December | January |

| October | January | February |

| November | February | March |

| December | March | April |

I’ve Been Paid. Do I Still Serve a Notice?

Regardless of project type (public or private), if you receive payment for a given month’s furnishing, prior to the notice deadline, you don’t need to serve the notice for those furnishings. Back to our example, if you are paid for April before the July notice deadline, then you can skip the notice in July.

Navigating Texas Notices Can Be Confusing – We Can Help

Understanding which notice to serve for each month’s furnishings, whether it’s a Texas notice of non-payment, a prelien notice, or a notice of intent to lien, can be quite confusing. Fortunately for you, our experts are Texas-savvy and ready to tackle the puzzle for you. Contact us today!