The Impact of Debtor Name Errors in UCC Financing Statements

Perfection of a security interest involves drafting and executing a sound security agreement, properly filing a UCC Financing Statement and ensuring the filing complies with Article 9 of the Uniform Commercial Code. When preparing a UCC filing, minor deviations in the name of the debtor can prevent a security interest from being perfected. Creditors may assume it is enough to simply conduct an online search to determine the correct spelling of a debtor’s legal name. However Article 9-503 (a) states that for a registered entity one must obtain the organic public record. Minor discrepancies coupled with strict state search logic can add up to a costly mistake.

Unperfected Security Interest

Let’s take a look at a few cases where the creditor failed to perfect their security interest, because searches conducted using the jurisdiction’s search logic did not reveal their UCC filing.

Jurisdiction: Nebraska

Case: EDM Corporation, doing business as EDM Equipment, doing business as NOVI, LLC, Debtor

Hastings State Bank, Plaintiff-Appellant v. Thomas D. Stalnaker, Chapter 7 Trustee of EDM Corporation

Verdict: The Court of Appeals for the Eighth Circuit affirmed the bankruptcy court’s ruling that the bank’s financing statement was “insufficient due to the addition of d/b/a” as part of the debtor’s name.

The bank listed the debtor’s name on the UCC filing with both the debtor’s public record and the d/b/a names. The debtor’s name was EDM Corporation and its d/b/a was EDM Equipment. The bank used a non-standard-form financing statement and listed the debtor as “EDM Corporation d/b/a EDM Equipment.” Subsequently, two separate lenders failed to turn up the financing statement when conducting UCC searches. The court noted that the standard-form financing statement expressly indicated not to include a d/b/a or other extraneous information in the field for the debtor’s name. The court emphasized the importance of putting in the exact public record name of the debtor – no more and no less.

Jurisdiction: Idaho

Case: Wing Foods, Inc., Debtor. Bankruptcy Estate of Wing Foods, Inc., by and through its Chapter 7 Trustee, Gary L. Rainsdon Plaintiff, vs. CCF Leasing Company and B S & R Equipment Company, Defendants.

Verdict: The court determined the UCC Financing Statement was “fatally flawed” and as a result, the debtor was permitted to avoid the creditor’s security interest.

The creditor, CCF Leasing Company, leased equipment to Wing Foods, Inc. The creditor took steps to perfect a security interest by filing the UCC; unfortunately, the financing statement listed the debtor’s name as “Wing Fine Food.” The court found that the difference in the name was seriously misleading because a UCC search, using the jurisdiction’s search logic, would not have revealed the financing statement. Because the filing was seriously misleading, the court ruled that Wing Foods, Inc. was able to avoid CCF Leasing Company’s security interest in its Chapter 7 bankruptcy.

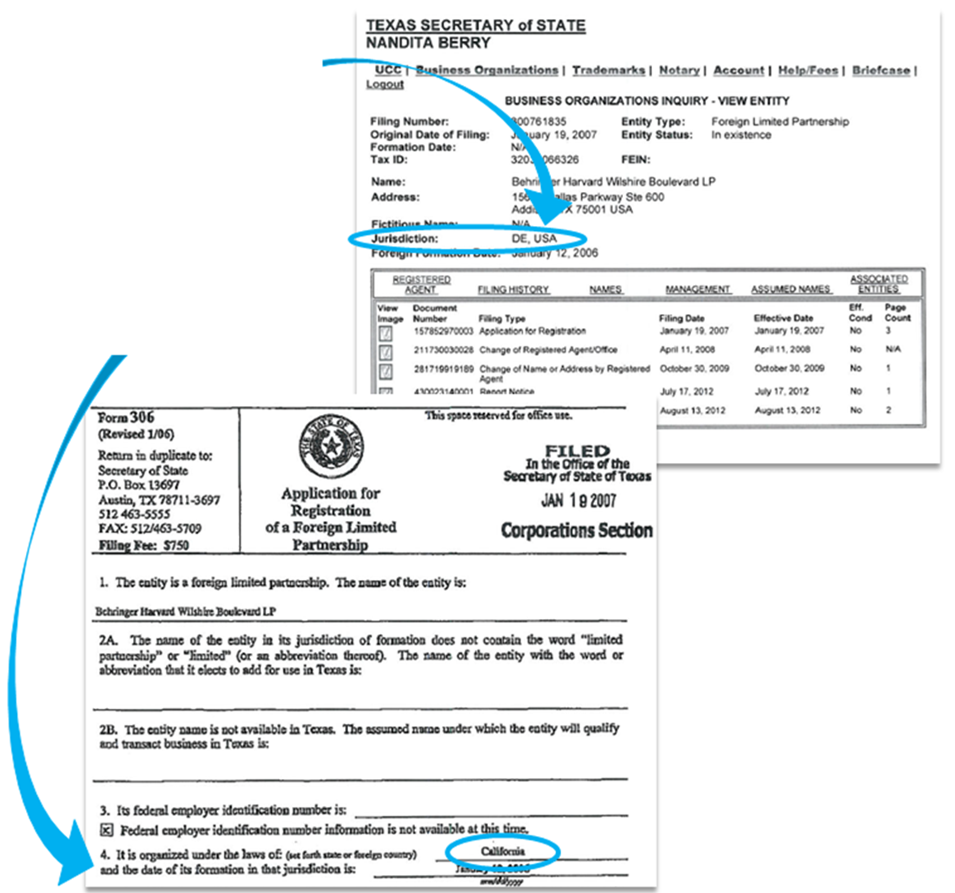

Jurisdiction: Texas

Case: In re JIM ROSS TIRES, INC.; dba HTC Tire Pro; dba HTC Tires & Automotive Centers, Debtor(s).

Verdict: The court found the listing of the debtor’s name “seriously misleading” because the search logic used for UCC searches in the state would not have revealed the financing statement.

On the UCC Financing Statement, the creditor listed the debtor by including both the debtor’s legal name and d/b/a – “Jim Ross Tires Inc. DBA HTC Tires and Automotive.” The creditor argued their security interest was perfected, because their filing could be located using a “non-standard wild card search”; unfortunately for the creditor, the court did not agree with their argument. “Accordingly, the Court finds that the Financing Statements are ineffective to grant security interests in Debtor’s collateral. Although this result is harsh, the Court must examine the result in the context of claims between competing creditors.”

Jurisdiction: Georgia

Case: Receivables Purchasing Co., Inc. v. R&R Directional Drilling, L.L.C.

Verdict: The appeals court affirmed the trial court, which determined the creditor did not have a security interest, because the financing statement was seriously misleading.

The creditor in this case simply added a space in the name of the debtor listing it as “Net work Solutions, Inc.” The creditor requested the Georgia Superior Court Clerks Cooperative Authority (GSCCCA) perform a search: “The GSCCCA did a certified search under the correct name Network Solutions, Inc. The Search did not reveal (debtor’s) financing statement, which…was filed incorrectly under Net work Solutions, Inc.”

Avoid this UCC Filing Mistake

While some creditors attempt to search online for a debtor’s business name, minor alterations to the name or the inclusion of a d/b/a could be fatal to the filing. We recommend you obtain the debtor’s corporate legal name from the Articles of Incorporation filed with the state and monitoring the entity’s name for any subsequent changes. In addition to confirming your debtor’s corporate legal name, it is important understand the search logic used in the state because including a space where one does not belong or changing “and” to “&” in the debtor’s name may be enough to render a UCC filing ineffective.