How Their UCC Filing Blunder Can Make You a Better Credit Manager

By now you have likely read thousands of articles and heard just as many news reports about JP Morgan’s “accidental UCC-3 Termination” – perhaps not thousands, but it was a widely covered topic in 2015. After all, accidentally terminating a UCC filing made JP Morgan an unsecured creditor – a $1.5 billion unsecured creditor.

Background

Here’s the unofficial “CliffsNotes®” version of what happened. (You can find full text of the case here) General Motors Corporation (GM) had two separate finance agreements with JP Morgan Chase Bank (JP Morgan). One agreement was for $300 million (a synthetic lease) and the other was for $1.5 billion (a term loan), both agreements were secured by different collateral and there was a UCC-1 filed for each.

GM paid off the $300 million, and subsequently asked their counsel to prepare the UCC-3 Termination. A representative with GM’s counsel ran a UCC search to locate the financing statement to be terminated, three results were returned with the search and the representative included all three with the termination filing.

Unfortunately, of the three filings included, one was the term loan for $1.5 billion which had not been paid in full.

The drafted paperwork was reviewed by GM’s counsel and forwarded to JP Morgan’s counsel, who also reviewed it – even signed a few documents – and the paperwork was then filed, “unknowingly terminating” JP Morgan’s security interest in the $1.5 billion.

None the wiser, until…GM filed for bankruptcy protection. Once the petition was filed, JP Morgan discovered the $1.5 billion unsecured debt and heads began spinning.

It was Simply an Accident, Right?

Yes, it was an accident, but no, it’s not simple. After GM filed for bankruptcy, and the unsecured debt came to light, JP Morgan advised the creditor’s committee that the UCC securing the $1.5 billion was terminated accidentally. (Even GM allegedly said they never intended to terminate this filing)

Through lengthy hearings and court of appeals processes, it was determined that whether the termination filing was intentional was irrelevant, because the termination was executed and therefore, the security interest was extinguished.

Don’t “Pull a JP Morgan”

When I say, don’t “pull a JP Morgan” I mean, don’t sign something without proper review – it doesn’t matter how many people reviewed it before you, if you are going to sign something, review it.

In this case, several parties “reviewed” and signed off on these documents, but clearly no one truly reviewed the documents, they simply relied on a belief that the person before them reviewed it. There was a checks/balance system in place, but that only works if the parties actually do the checks!

You Will Be a Better Credit Manager

Keep this case in mind when you establish a new UCC filing process or modify your current process. UCC filing requires concise & correct information and, as in the JP Morgan case, leaves very little to no room for error.

It’s important to correctly identify the involved parties, the collateral etc., but it’s crucial to review a filing carefully before recording it. Don’t leave the task of UCC filings to one person. At the very least, have one person prepare the documents and a separate person carefully review the documents before filing.

When I was in grade school, our teacher would have us exchange our papers with a classmate to proofread, make changes, correct errors, before turning the document in for a grade. Same thing should go for financing statements: Review. Review. Review. And then review it again.

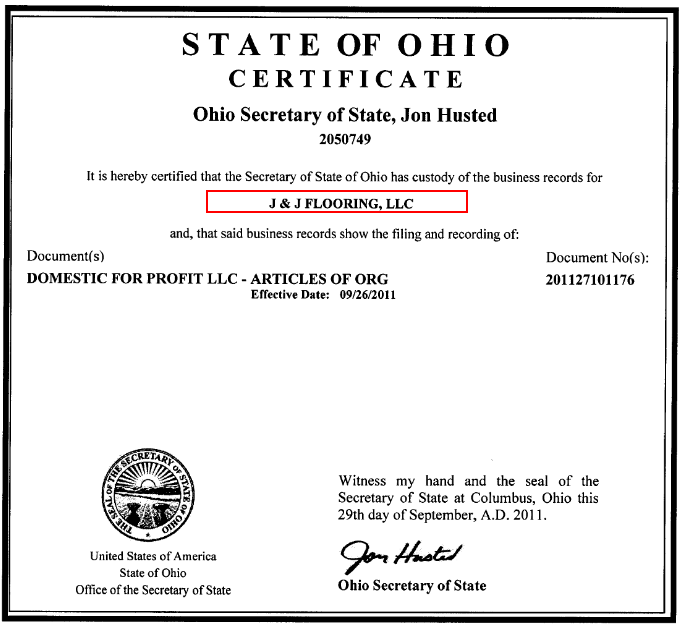

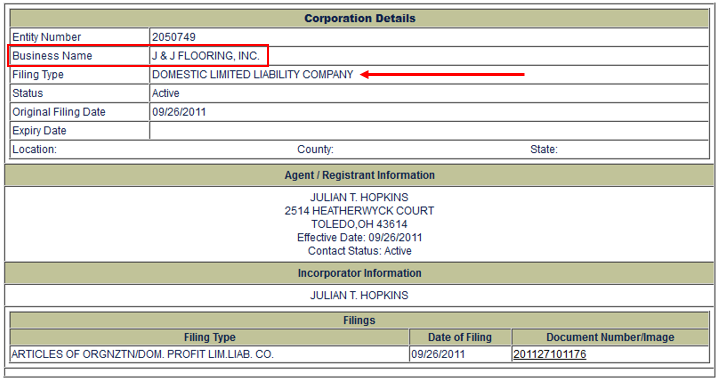

Under “filing type” the state indicates J & J Flooring is a Limited Liability Company, which is commonly referred to as an “LLC”.

Under “filing type” the state indicates J & J Flooring is a Limited Liability Company, which is commonly referred to as an “LLC”.