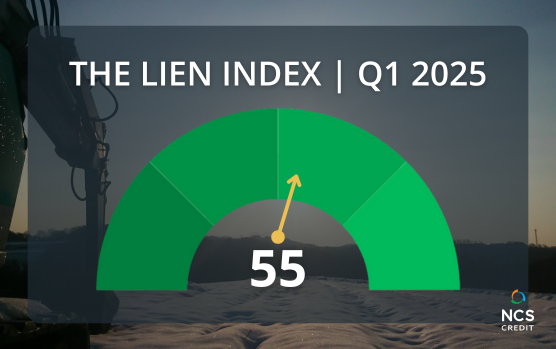

NCS Credit’s Lien Index Ends Q1 2025 at 55, Down 8% from Q4

Lien Index down 5 points to 55 from revised Q4 score of 60*. Mechanic’s Lien activity has declined, but is forecasted to increase in coming quarters.

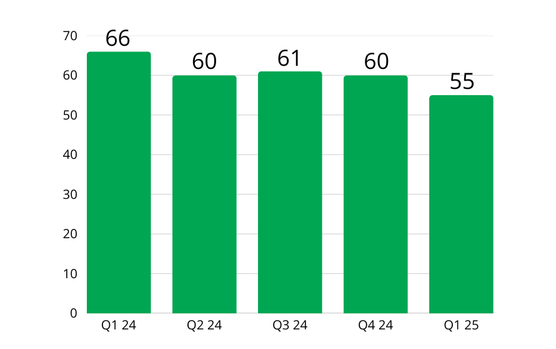

National Mechanic’s Lien Activity

The Lien Index ended Q1 2025 at 55; an approximate 8% decline in activity from Q4 2024 and 17% decline compared to Q1 2024. This is the lowest the Index has been in the last two years, with Q2 2023 also coming in at 55.

Thus far, 2025 has been marred by uncertainty. Chapter 11 bankruptcies are up 20% over 2024, and tariffs are front of mind, while the stock market tries to find footing. Fortunately, lien activity did decline in Q1, some of which is attributed to the cyclical nature of construction projects.

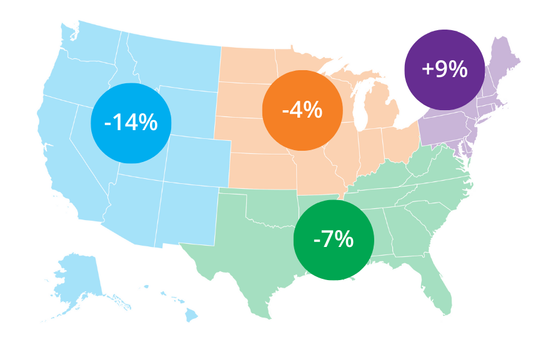

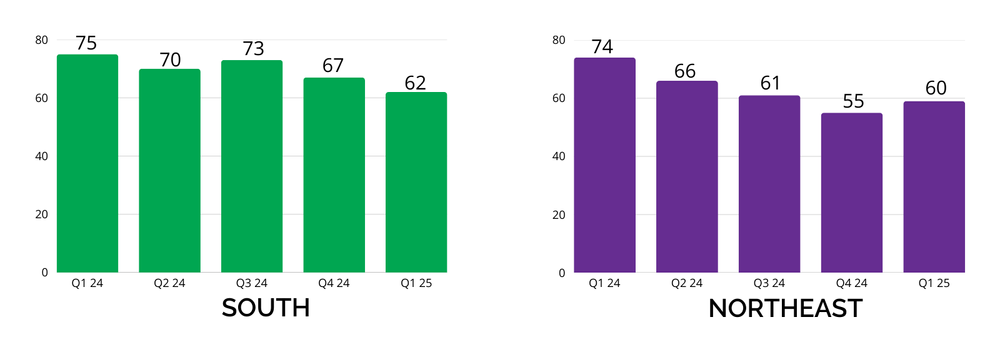

Regional Mechanic’s Lien Activity

The South and Northeast led the country in lien activity in Q1, with the Northeast experiencing a 9% increase in liens over the previous quarter. Activity in the South did decline 7%, though remains well above 50, as slow payments continue.

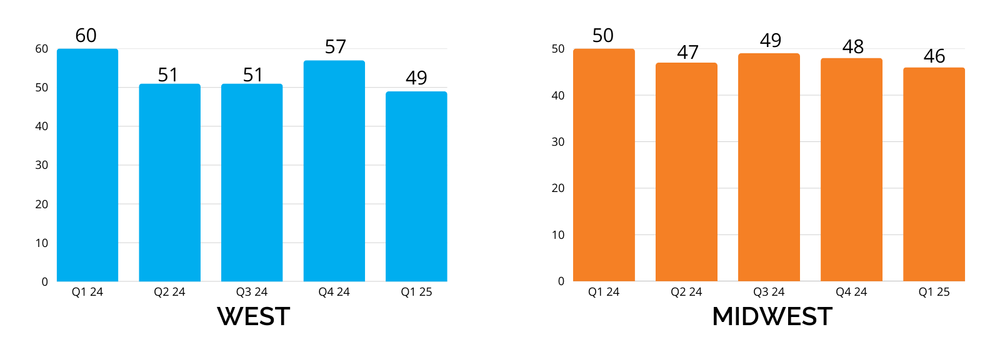

Lien activity in the Midwest has steadily declined over the last 3 quarters, down 4% over Q4 2024.

Rounding out national activity, the West dropped significantly, coming in 14% lower than last quarter. However, there is an anticipated increase as communities begin rebuilding from the tragic wildfires.

States with Highest Lien Activity

The top 5 states for lien activity were (in order of volume): Texas, Florida, California, Nevada and New York.

Top 3 States by Region

- West: California, Nevada, Colorado

- Midwest: Iowa, Ohio, Michigan

- South: Texas, Florida, Georgia

- Northeast: New York, Massachusetts, New Jersey

Looking Forward

As we progress through 2025, payment challenges will remain a significant concern for businesses across the supply chain, affecting everyone from material suppliers to contractors. We do expect lien filings to increase as material prices are anticipated to skyrocket, straining open credit terms and pinching cash reserves.

Cash flow disruptions and delayed payments are expected to persist, placing considerable financial strain on companies. The situation is worsened by slow-paying clients and creditors facing their own financial difficulties. In addition, the uncertainty surrounding tariffs and the broader global economic climate is fueling further instability, amplifying unpredictability across the industry.

In today’s uncertain environment, it’s essential for businesses to take proactive steps to protect their financial interests. Mechanic’s liens and UCC filings offer valuable legal recourse in the event of non-payment. These safeguards provide a clear path to securing payment for your work, even in turbulent times. Act now to fortify your business against the challenges that lie ahead.

Industry Experts

The Architecture Billings Index (ABI) experienced another quarter of declining billings. “Clients are increasingly cautious about starting projects due to uncertainty over future trends in interest rates and building materials costs, as well as the potential for an economic slowdown,” said Kermit Baker, PhD, Hon. AIA, AIA Chief Economist. “Unfortunately, this softness in firm billings is likely to continue as indicators of future work remain weak, however, the average project backlog at firms stands at a reasonably healthy 6.5 months, offering a bit of a buffer if future project work continues to remain soft.”

Associated Builders and Contractors (ABC) reported its Backlog Indicator ended Q1 at 8.5 months, however, this was prior to the tariff announcement. “Backlog increased in March and contractors remained optimistic regarding the future, but this largely reflects contractor activity and sentiment prior to April 2, when the most consequential economic policy in several decades was announced,” said ABC Chief Economist Anirban Basu. “Approximately 80% of ABC contractors surveyed indicate that suppliers have notified them of tariff-related materials price increases, and nearly 20% of contractors surveyed had projects paused or interrupted because of tariffs during March,” said Basu. “These tariffs have already materially diminished the outlook for construction activity in 2025. Many businesses are poised to delay or even cancel planned capital investments given the current business environment and daily market convulsions. Conditions will likely deteriorate further if elevated tariff rates remain in place for any meaningful length of time.”

The Dodge Momentum Index grew 6% in January and 1% in February, but declined 7% in March. “Increased uncertainty around material prices and fiscal policies may have begun to factor into planning decisions throughout March,” stated Sarah Martin, Associate Director of Forecasting at Dodge Construction Network. “While planning data has weakened across most nonresidential sectors this month, activity remains considerably higher than year-ago levels and still suggests steady construction activity in mid-2026.”

Epiq Bankruptcy reported Chapter 11 filings were up 20% in March from previous year. Michael Hunter, Vice President of Epiq AACER, stated “The 20 percent rise in commercial Chapter 11 filings to 733 in March 2025, up from 611 last year, signals persistent economic pressure…Meanwhile, credit card delinquencies have hit a near 10-year high, driven by rising interest rates and consumer debt burdens.” Further, ABI Executive Director Amy Quackenboss said, “Inflation, elevated interest rates, tighter lending terms and geopolitical tensions are creating more challenges for distressed consumers and businesses looking to alleviate their growing debt loads.”

*Nationwide, recording offices manage a backlog of requests. The Index data is adjusted and revised accordingly.