Georgia Bankruptcy Court deemed creditor’s UCC filing misleading

Who enjoys a good ol’ mystery game? Today’s mystery is why a Georgia Bankruptcy Court deemed one creditor’s UCC filing seriously misleading, thus making the creditor’s security interest unperfected. First, we’ll go through the facts of the case, then review the requirements under Article 9, and then the big reveal: why was the UCC seriously misleading!

Facts of Case

In re Wastetech, LLC, Bankr. Court, ND Georgia 2019

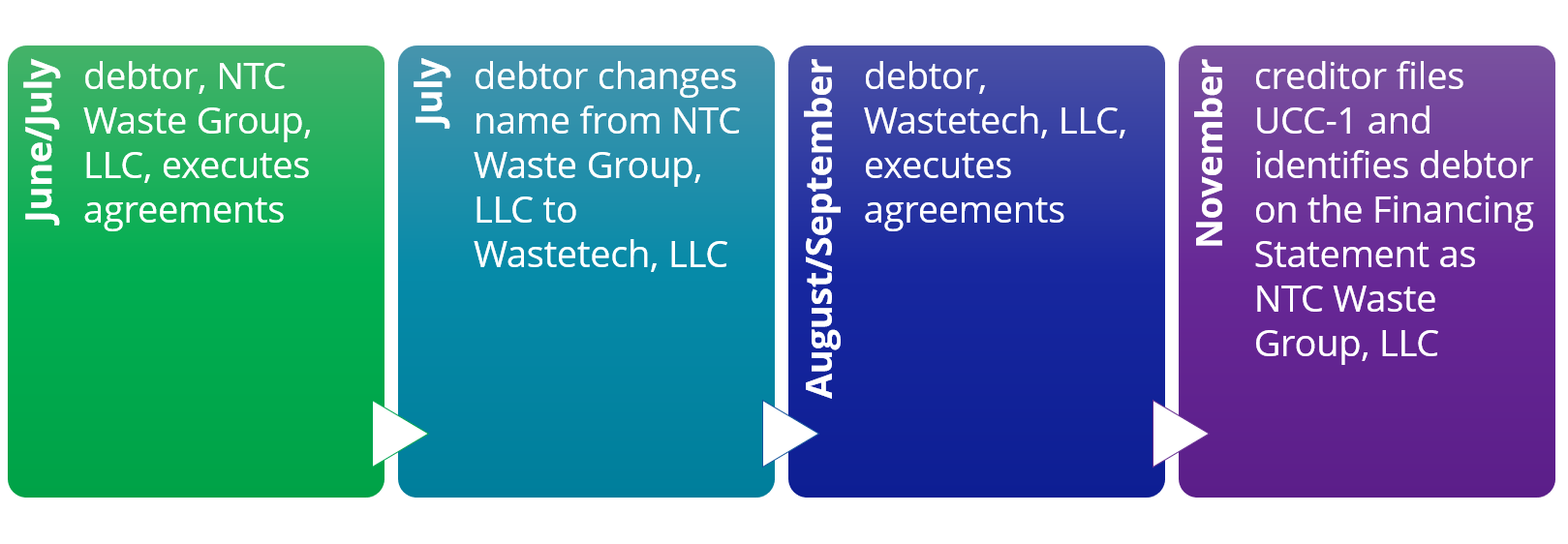

In 2017, the debtor executed six agreements granting a secured interest to the creditor. The six agreements were executed on the following dates in 2017: June 13, July 6, July 19, August 3, August 18, and September 26.

The Debtor’s Name Change

Smack in the middle of these six agreements, on July 27, 2017, the debtor changed its name from NTC Waste Group, LLC to Wastetech, LLC.

The Creditor’s UCC Filing

On November 14, 2017, the creditor filed a UCC-1 Financing Statement. The creditor identified the debtor on the Financing Statement as NTC Waste Group, LLC. Within the Financing Statement, the creditor also provided the following collateral description:

“Certain future receivables sold by said business seller and purchased by Crown Funding Group, Inc., as buyer, pursuant to that certain purchase and sale of future receivables agreement between seller and purchaser dated 8/7/2017 (the “agreement”).”

Timeline of Pertinent Events

The Debtor Files for Bankruptcy & Trustee Begins the Search

February 13, 2018, the debtor filed for bankruptcy protection. After the bankruptcy filing, the bankruptcy trustee set out to identify the creditors with UCC filings in place.

The trustee searched for UCC filings by two variations of the debtor’s current name: “Wastetech” and “Wastetech, LLC”. The trustee’s searches did not reveal any UCC filings. The trustee then submitted to the court that it also searched by the debtor’s former name (NTC Waste Group, LLC), which did reveal a UCC filing. Searching got a bit technical, here’s an excerpt from the court decision:

“… the Trustee recently conducted several UCC index searches through the GSCCCA database using the Debtor’s correct name as well as its former name… According to the Affidavit, statewide “searches using the search terms `Wastetech’ or `Wastetech LLC’ did not lead to finding the Financing Statement.” Only searches using the former name of the Debtor produced the Financing Statement.”

But wait, there’s more! The trustee was certainly thorough.

“Further searches conducted using the standard search logic in the Debtor’s name through the GSCCCA database in the Coweta County UCC Index along with a stem search for the Debtor’s name also failed to return the Financing Statement, though UCC-1’s for another entity were disclosed. Finally, additional statewide stem searches using the Debtor’s name did not disclose the Financing Statement. Based on these results, the Trustee through counsel states that ‘a search of the Coweta County UCC Index, and the Georgia Statewide UCC Index, using a debtor name stem search in the GSCCCA database for the Debtor’s correct legal name of record did not disclose the Financing Statement.’”

No Safe Harbor

The search type described above was to prove the creditor’s Financing Statement didn’t appear under the “single exception” aka safe harbor. (The single exception, according to the court decision, is “a search of the records of the filing office under the debtor’s correct name, using the filing office’s standard search logic” which would disclose such financing statement.”)

Corporate Search & Public Organic Record Are Not the Same

The creditor argued “…that a search of the UCC records under “NTC” did produce the Financing Statement, and that a search of “wastetech” in the records of the Georgia Corporations Division led to Wastetech LLC, which was formerly known as NTC Waste Group, LLC…”

Yes, you read that correctly “Georgia Corporations Division” (a corporate search, not the public organic record).

The creditor cited several cases regarding effective UCC filings, despite the debtor name being incorrect. Unfortunately for the creditor, the cases cited all related to UCC filings that were filed PRIOR to a debtor’s name change. The creditor also tried to argue that it filed its UCC within 4 months of the debtor’s name change — but that’s not how it works. It appears the creditor wanted the 4 month window under Article 9-507(c) to apply, except that section applies to UCCs filed prior to a name change.

OH, and the Collateral Description

There was an issue with the creditor’s collateral description – which seems minor compared to the flurry of back & forth over the correct name of the debtor. Within the UCC-1 Financing Statement, the collateral description is “certain future receivables sold by said business seller and purchased…” But it did not please the court because the collateral description is specific rather than of a category.

“Had the description been “all future receivables of the Debtor,” it would have met the requirements under Section 11-9-108 by describing the collateral through category.”

The judge is ready to decide. Is the UCC filing seriously misleading?

The judge did not mince words in the decision. The creditor’s UCC filing was seriously misleading, which made the filing ineffective and the security interest unperfected.

“First, the Debtor’s name as listed in the Financing Statement is inconsistent with its legal name on the public record. Moreover, a search of the Georgia Superior Court Clerks’ Cooperative Authority’s Lien records for the Debtor’s correct name would not have disclosed the existence of the Financing Statement. Second, the Financing Statement does not indicate that it covers all assets or all personal property of the Debtor, and it fails to provide a description of, or reasonably identify, the Debtor’s Accounts Receivable that are subject to the Defendant’s security interest. Accordingly, the Financing Statement is seriously misleading, and perfection of the Defendant’s security interest in Debtor’s Accounts Receivable is legally ineffective.”

OK, So Maybe It’s Not a Mystery. Seriously.

I admit, as far as mysteries go this was kind of lame. I mean, given the facts of this case, is it really a mystery that the creditor was left with an ineffective Financing Statement, hanging out with unsecured creditors? Failing to correctly identify the debtor on the Financing Statement, relying on a corporate search versus the public organic record, and providing a poor collateral description? Definitely no mystery. I promise to craft a better mystery next time, until then, don’t be like this creditor!

- Always identify your customer by their name as it appears in the public organic record

- Public organic record and a corporate search are NOT the same thing

- Carefully review your collateral description

- After filing, conduct a reflective search to confirm the filing has been indexed properly