The U.S.’s Article 9 of the Uniform Commercial Code (UCC) and Canada’s Personal Property Security Act (PPSA)

The U.S.’s Article 9 of the Uniform Commercial Code (UCC) and Canada’s Personal Property Security Act (PPSA) are sets of law that govern commercial transactions between states and provinces.

The PPSA was largely modeled after the UCC.

Forms

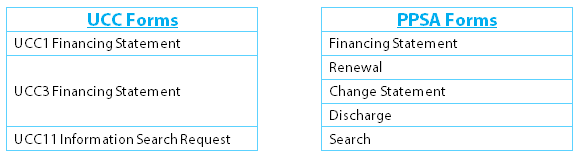

First, let’s take a look at the specific forms used when filing a UCC or registering a PPSA. It’s interesting to note, in the U.S. the UCC3 Financing Statement is used if a filing needs to be amended, continued or terminated. Whereas in Canada, a Renewal is used to continue a filing, a Change Statement is used to amend a filing and a Discharge is used to terminate a filing.

UCC and PPSA

In order to create a security interest you must:

- Have a signed Security Agreement and the security agreement must contain a granting clause and collateral description

- Record (US) or Register (Canada) the Financing Statement to make the security interest public record

- Notify the prior secured creditors in order to Establish Priority in Inventory

The Financing Statement does not require the debtor’s signature

UCC versus PPSA

Despite their overall similarities, there are significant differences between the UCC & the PPSA

- Individuals

- Under the UCC, verify the individual’s name with an unexpired driver’s license

- Under the PPSA, include the individual’s birthdate

- Establish Priority in Equipment

- Under the UCC you must record your filing within 20 days of your customer’s receipt of the equipment

- Under the PPSA you must register your filing within 15 days of your customer’s receipt of the equipment

- Where to File

- A UCC: for a registered entity the UCC is filed in the state of organization and the UCC for an individual is filed in the state of residence

- A PPSA: if the entity is registered in British Columbia, Ontario, or Saskatchewan, the PPSA is registered in the province of registration, otherwise the PPSA is registered in the province(s) in which the entity is registered and where goods are located

- Life of Filing

- In the US, the secured party’s filing is good for 5 years (in most states – WY filings are good for 10 years)

- In Canada, the secured party may choose a filing period from 1-25 years or “infinity”

PPSA

The PPSA allows for repossession upon default, much like the UCC, however, the PPSA provides a broader definition of default.

Default is the failure to pay or otherwise perform the obligation secured when due, or the occurrence of an event or set of circumstances that, under the terms of the security agreement, causes the security interest to become enforceable.

A secured party may take possession of and sell the collateral when the debtor is in default under the security agreement or when the collateral is at risk. The collateral is “at risk” if the secured party has reasonable grounds to believe the collateral has been or will be destroyed, damaged, endangered, disassembled, removed, concealed, sold, or otherwise disposed of contrary to the terms of the security agreement.

Remember Quebec did not adopt the PPSA. They have their own law called the Civil Code of Quebec. The most recognized difference between Quebec and PPSA law is the interpretation of the concept of chattel mortgage.

Editor’s Note: This content was originally published in August 2014. It has since been updated and revised for 2023.