In Some States, You Should Serve the Lender with the Preliminary Notice to Protect Your Mechanic’s Lien and Bond Claim Rights

The infamous first step to protecting mechanic’s lien and bond claim rights: serve the statutory preliminary notice. State statute not only dictates when your notice should be served and what information should be included in the notice, it also dictates who should receive a copy of the notice. Frequently, the project owner and/or the general contractor (GC) are required to receive a copy of the preliminary notice. But did you know a couple states require the lender also receive a copy of the preliminary notice?

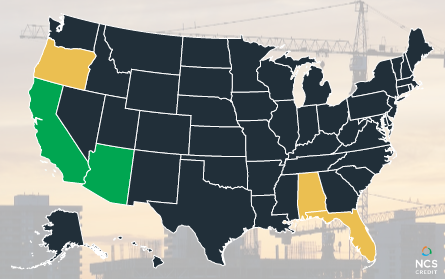

Definitely Serve the Lender with the Notice in These 2 States

Two states require serving the notice upon the lender and indicate serving the lender may improve the priority of your mechanic’s lien.

First up, Arizona and California. These states’ statutes explicitly identify the construction lender as a required party (emphasis added):

Ariz. Rev. Stat. Ann. 33-992.01 B. Except for a person performing actual labor for wages, every person who furnishes labor, professional services, materials, machinery, fixtures or tools for which a lien otherwise may be claimed under this article shall, as a necessary prerequisite to the validity of any claim of lien, serve the owner or reputed owner, the original contractor or reputed contractor, the construction lender, if any, or reputed construction lender, if any, and the person with whom the claimant has contracted for the purchase of those items with a written preliminary twenty day notice as prescribed by this section.

California statute says:

CA Civ Code 8200 (a) Except as otherwise provided by statute, before recording a lien claim, giving a stop payment notice, or asserting a claim against a payment bond, a claimant shall give preliminary notice to the following persons:

(1) The owner or reputed owner.

(2) The direct contractor or reputed direct contractor to which the claimant provides work, either directly or through one or more subcontractors.

(3) The construction lender or reputed construction lender, if any.

Consider Serving the Lender with the Notice in These 3 States

Then there’s Alabama, Florida, and Oregon.

There is case law in Alabama which supports serving the lender with the notice, though statute doesn’t specifically identify it as a requirement.

“The building industry today is operated on the basis of borrowed money, i.e., construction financing. Practically every corporation or would-be home owner must borrow. The practice in the industry has typically been that the construction loan funds will not be distributed in a lump sum. Rather, the funds are advanced from time to time as construction progresses, upon the lender’s ascertainment (by the use of monitoring procedures such as vouchers and on-site inspections) that the work is indeed being completed or the supplies being furnished. This procedure allows the lender to actually corroborate the expenditures.

Because of the practices in the construction industry, we hold that from this day forward, public policy dictates that the same written notice that is required to be given to the owner must also be given simultaneously to the construction lender, if the lender’s identity can reasonably be obtained. We note that it would not be that difficult to obtain the identity of the construction lender, because the lender’s mortgage would be on record in the office of the judge of probate. This notice would give the construction lender, as well as the owner, the opportunity to insure that the mechanics and materialmen are paid out of the remaining contract funds, that any potential liens are satisfied, and that the property is not encumbered.” – Bailey Mortg. Co. v. Gobble-Fite Lumber Co.

In Florida, if the lender is listed on the Notice of Commencement, you should consider sending them a copy of the preliminary notice.

F.S. Title 40, Section 713.06 (d) A notice to an owner served on a lender must be in writing, must be served in accordance with s. 713.18, and shall be addressed to the persons designated, if any, and to the place and address designated in the notice of commencement. Any lender who, after receiving a notice provided under this subsection, pays a contractor on behalf of the owner for an improvement shall make proper payments as provided in paragraph (3)(c) as to each such notice received by the lender. The failure of a lender to comply with this paragraph renders the lender liable to the owner for all damages sustained by the owner as a result of that failure…

Regardless of where that party falls in the contractual chain, if they appear on the Notice of Commencement, it’s in your best interest to serve them with a copy of the preliminary notice.

Oregon’s statute doesn’t say the lender is required; however, if you serve the lender your mechanic’s lien may have greater priority.

ORS 87.025 (3) No lien for materials or supplies shall have priority over any recorded mortgage or trust deed on either the land or improvement unless the person furnishing the material or supplies, not later than eight days, not including Saturdays, Sundays and other holidays as defined in ORS 187.010, after the date of delivery of material or supplies for which a lien may be claimed delivers to the mortgagee either a copy of the notice given to the owner under ORS 87.021 to protect the right to claim a lien on the material or supplies or a notice in any form that provides substantially the same information as the form set forth in ORS 87.023.

Best Practice: Serve All Parties with the Notice, even if the Notice Isn’t Required

We are firm believers in serving the preliminary notice upon all parties within the contractual chain. Why? Glad you asked – let’s take a look.

Ensure Compliance with Statute

Mistakes happen. One of the most common obstacles in securing lien and bond claim rights is knowing which parties are actually in the contractual chain; gathering job information is tough.

How many times have you reviewed project information and discovered you only have information for the project location and your customer? Your customer tells you “I’m a contractor on the project” – are they the GC or are they a subcontractor (sub)? If you think they’re a sub and opt to not send the preliminary notice, then later find out they were the GC and required to receive a copy of the notice. An easy way to avoid “Oops, I didn’t know I needed to serve the lender” is if you serve everyone in the contractual chain.

Become a Payment Priority

Preliminary notices are harmless (unless, of course, you don’t send them) and an excellent way to promote transparency while establishing your place as a payment priority. By notifying everyone of your involvement, parties know your company name, how to get in touch with you, and what you are furnishing to the project.

Think of it this way: what if something goes awry with the GC and the owner begins remitting payment direct to subcontractors and various suppliers. Don’t you want to be front of mind for the owner? Wouldn’t it be nice if the owner had a notice from you (which includes your contact information) and they could speak with you directly to make payment arrangements?

Just think of all the subcontractors and suppliers the owner doesn’t know about – how quickly are those folks going to get paid? Not only are they unlikely to get paid, but it’s also more likely they will have to proceed with a mechanic’s lien or bond claim.

Serve the Notice, Every Time

If I had to choose between the cost of a preliminary notice or the cost of lost lien rights, I would choose the preliminary notice. Every. Single. Time.

Not sure who the lender is? We can help. Our experts are knowledgeable and ready to handle lender searches for you – contact us today!