What You Should Know about Securing Utah Mechanic’s Lien and Bond Claim Rights

Furnishing to a construction project in the Beehive State? Well, today’s post is just for you as we explore Utah mechanic’s lien and bond claim rights.

Utah Mechanic’s Lien Rights

If you are furnishing to a private construction project, you should file a preliminary notice with the State Construction Registry (aka the SCR) within 20 days from first furnishing. The SCR is an online database for required notices for commercial, public, and residential construction projects.

We are often asked “Can I send a late notice?” Yes, for projects in Utah, a late preliminary notice may be filed; however, the lien will only be enforceable for materials and services furnished 5 days or more after the notice is filed.

Need to proceed with a mechanic’s lien? You should file the lien within 90 days from the filing of the notice of completion or within 180 days from final completion of the original contract if no notice of completion has been filed. And you should serve a copy of the lien upon the owner within 30 days from filing the lien.

In the unlikely event you need to proceed with suit to enforce your mechanic’s lien on a commercial project, you should file suit within 180 days from filing the lien.

If the private project is residential, you should familiarize yourself with the Residential Lien Recovery Fund. If the owner can prove compliance with the requirements of the Residential Lien Recovery Fund, the lien will have to be released. The claimant can apply to the fund for payment of the claim provided a judgment has been obtained against the debtor and the claimant is registered with the fund. Suit to enforce a claim under the Lien Recovery Fund must be filed within the earlier of 180 days from filing the lien or 270 days from completion of the original contract.

Have you heard of the Preconstruction Service Lien? This lien is available to those who provide designing or planning services prior to construction. If you provide these services, you should file a Notice of Preconstruction Service on the database within 20 days from first performing service, then file the Preconstruction Service Lien within 90 days from completion of the preconstruction service, and file suit to enforce the lien within 180 days from filing the Preconstruction Service Lien.

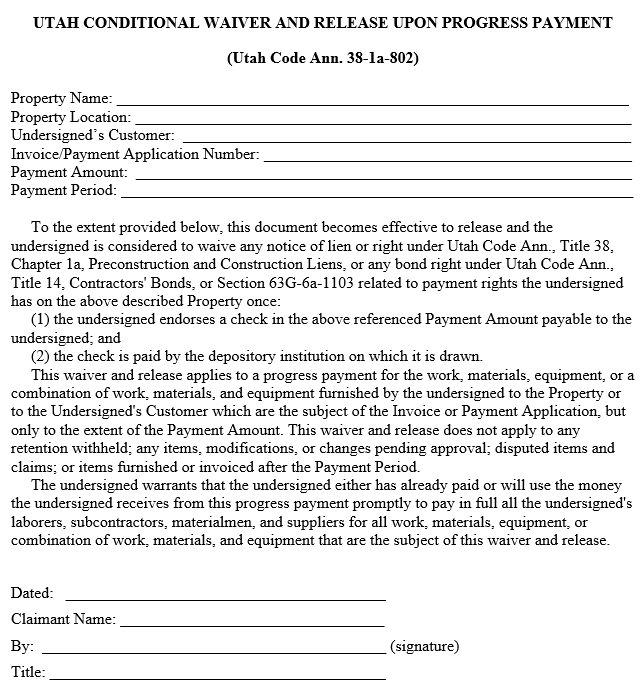

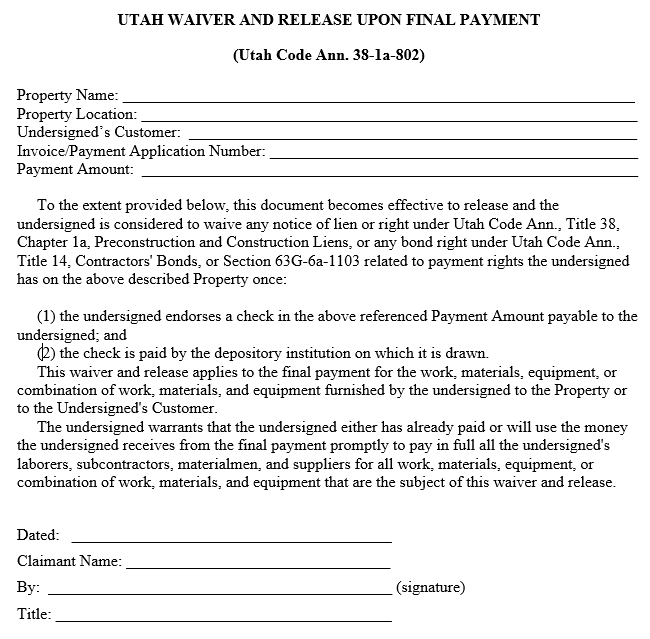

Utah Lien Waivers

Utah is one of about a dozen states that has specific lien waiver requirements. Here’s a Utah Waiver and Release Upon Progress Payment followed by a Utah Waiver and Release Upon Final Payment.

Utah Bond Claim Rights on Private Projects

Yes, you read that right, a payment bond may be issued for a private project in Utah (Utah Code Ann. 14-2). Generally, payment bonds are required on commercial projects exceeding $50,000, and if the owner fails to require a payment bond, the owner is liable to the claimant. To secure bond claim rights, you should file your preliminary notice with the SCR within 20 days from first furnishing.

There is no statutory provision requiring you to serve a bond claim. However, it is recommended you serve a bond claim upon all parties within 90 days from your last furnishing. If you need to proceed with suit to enforce the bond claim, you should file suit after 90 days from your last furnishing, but within 1 year from last furnishing.

Utah Bond Claim Rights on Public Projects

The process for securing bond claim rights on a public project is nearly the same as it is for private projects. You should file your preliminary notice with the SCR within 20 days from first furnishing or within 20 days from the filing of a notice of commencement, whichever is later. A late preliminary notice may be filed; however, the bond claim will only be enforceable for materials and services furnished 5 days or later after the notice is filed. A preliminary notice is not required if a notice of commencement is not filed.

Generally, there is no statutory provision requiring a bond claim notice. It is recommended to serve a bond claim notice upon all parties within 90 days from last furnishing. If the public entity fails to require a payment bond, the public entity is liable to the claimant and shall make payment to the claimant upon demand. Serve bond claim notice upon the public entity within 90 days from last furnishing.

File suit to enforce the bond claim after 90 days from last furnishing, but within 1 year from last furnishing. If the public entity fails to require a payment bond, file suit against the public entity within 1 year from last furnishing.

Retainage on Utah Construction Projects

Utah’s statute dictates retainage may not exceed 5%:

(3) (a) Notwithstanding Section 58-55-603, the retention proceeds withheld and retained from any payment due under the terms of the construction contract may not exceed 5% of the payment:

(i) by the owner or public agency to the original contractor;

(ii) by the original contractor to any subcontractor; or

(iii) by a subcontractor.

(b) The total retention proceeds withheld may not exceed 5% of the total construction price.

(c) The percentage of the retention proceeds withheld and retained pursuant to a construction contract between the original contractor and a subcontractor or between subcontractors shall be the same retention percentage as between the owner and the original contractor if:

(i) the retention percentage in the original construction contract between an owner and the original contractor is less than 5%; or

(ii) after the original construction contract is executed but before completion of the construction contract the retention percentage is reduced to less than 5%.

Generally, any retention should be released pursuant to a billing statement from the contractor within 45 days from the date the owner receives a billing statement from the contractor, the date of final acceptance or the date a certificate of occupancy is issued, or the date the contractor accepts final payment, whichever is later.

Utah’s Prompt Pay Statute

The prime contractor should release progress payments to its subcontractors within 30 days after the owner remits payment to the prime. For final payments, the prime contractor should release funds to its subs 10 days after it receives final payment from the owner. [Utah Code Ann. 13-8-5]

Subcontractors should release progress payments to its subs/suppliers within 30 days after it receives payment from the prime. And, similar to prime contractors, the subcontractor should release final payments within 10 days after it receives its final payment from the prime contractor. [Utah Code Ann. 58-55-603]

Questions about securing Utah mechanic’s lien or bond claim rights? Contact us and speak with a specialist today!