Credit Research Foundation Survey: The Use & Impact of Securitization on A/R During the Pandemic

Originally published in The Credit Research Foundation’s Perspective newsletter (June 2021)

The Credit Research Foundation recently surveyed their membership on the use and impact of securitization (UCCs, mechanic’s lien, etc.) on accounts receivable during the pandemic. The survey explored the use of securitization as a risk mitigation tool.

“I Believe There Will Be an Increase in Bankruptcies During 2021.”

Unsurprisingly, 88% of respondents believe there will be an increase in bankruptcies in 2021. In general, 2020 saw a low rate of bankruptcies, in fact Epiq reported bankruptcy filings across all chapters were at their lowest point since 1986. However, commercial Chapter 11 bankruptcies continued to rise year over year, with a 29% increase in 2020, for a total of 7,128 filings. Forecasts indicate bankruptcy filings will increase in 2021, with a predicted spike in Q3 2021.

Why Will Bankruptcy Filings Increase in 2021?

This is certainly a question on many credit professionals’ minds as the challenges of the economy, government stimulus and indebtedness in the marketplace plague the overall portfolio risk of many organizations. Additionally, Congress extended Sub-Chapter 5 of the Bankruptcy Code (small business) and the grace period to file under the extended debt levels ($7.5 million) an additional year, which now expires in March of 2022. Given these factors there seems to be an awareness to the potential for at least certain segments of the economy to file for bankruptcy. Anecdotally, conversations from many members of the Foundation have all eyes on Q3 and Q4 of 2021 as a pivotal and anticipated point for the next level of bankruptcy activity.

In an earlier NCS survey, 62% of respondents were actively monitoring their customers for bankruptcy. Continue to monitor your customers, and if there is a bankruptcy, ensure to complete your Proof of Claim by the bar date.

“Our Company Has Been an Unsecured Creditor in a Bankruptcy and Recovered Less Money Than Secured Creditors.”

An overwhelming 90% of respondents have suffered as unsecured creditors in a bankruptcy, watching from the sidelines as secured creditors recovered payments in full. These losses are preventable and at minimal cost. Secured transactions are your greatest defense against customer failure. Time & time again, we see secured creditors receive payment in full while unsecured creditors receive pennies on the dollar.

For example, Katy Industries, a leading manufacturer, importer, and distributor of commercial cleaning and consumer storage products, filed for bankruptcy when it was unable to meet the obligations of its creditors, with nearly $56 million of debt. In this case, secured creditors recovered the total amount of allowed claims (100%) while unsecured creditors faced a recovery rate of only 9.6%.

Another example comes from the healthcare industry. Holmes, Inc., provided health & wellbeing programs nationwide. When it filed for bankruptcy protection, its capital deficit was $31.5 million. According to the bankruptcy plan, secured creditors were to receive 100% of their claims and unsecured creditors were to receive approximately 3.5% of their claims.

Need more? In the Hostess bankruptcy, secured creditors recovered 100% and unsecured creditors recovered 0. In Kodak’s bankruptcy, secured creditors recovered 100% and unsecured creditors recovered 4-5%. Then there was Uno, where secured creditors received 100% and unsecureds received 13%. And HomeBanc Corp. distributed 100% of claims to secured creditors and unsecureds recovered anywhere from 1-10%.

“Our Company Currently Secures Our Accounts Receivable, Either in Full or Partially.”

83% of respondents currently secure their A/R. For the 17% who don’t currently secure A/R, the top two cited reasons are concerns about customer reaction and the costs associated with securing A/R, followed by no significant write-offs, no need, and reliance on 503(b)9 claims. A respondent from the manufacturing industry stated they do not secure A/R because “We have an 85% recovery rate as a Critical Vendor in our industry.”

Let’s circle back to the top two cited reasons for not securing A/R: concerns about customer reaction and costs. First, it’s OK to be nervous about how your customer will respond to your request for a signed Security Agreement (needed to file UCCs) or your customer’s reaction when they receive a preliminary notice (needed to secure mechanic’s lien rights) via certified mail. But rest assured, these are traditional business practices that do not harm your customer’s creditworthiness or cost your customer a dime. UCCs and preliminary notices/mechanic’s liens secure your right to recover payment in the unlikely event your customer defaults or files bankruptcy. If your customer never defaults or files for bankruptcy, it’s as though the UCC/lien never existed.

As for the costs associated with UCCs and preliminary notices/mechanic’s liens, they are nominal compared to the hundreds of thousands of dollars you could lose as an unsecured creditor. These are general numbers, but a blanket UCC filing may cost around $100 and a PMSI filing with search & notify may cost around $175, and the protection is in place for 5 years. As for preliminary notices/mechanic’s liens, let’s focus on the preliminary notice. Why? Because research shows 97.3% of the time a preliminary notice is enough to get you paid. Generally, a preliminary notice may cost around $60 per project. Now, mechanic’s liens may have a higher price tag ($500+) but again, when compared to what you could lose, it’s a small price to pay.

Lastly, I do want to mention that 503(b)9 claims are a great resource; however, there are some pitfalls. The bankruptcy code was amended in 2005 to include a new administrative claim: 503(b)(9). With the addition of 503(b)(9) claims, some creditors became complacent. The availability of a 503(b)(9) claim seemed to misleadingly allay creditor concerns, “Nah, I don’t need UCC filings. We just file a 503(b)(9) to get paid.” This somewhat false sense of security can easily cost creditors millions of dollars.

Under 503(b)(9), creditors may file a claim for “the value of any goods received by the debtor within the 20 days before the date of commencement of a case under this title in which the goods have been sold to the debtor in the ordinary course of such debtor’s business.”

As you can imagine, there are challenges with 503(b)(9) claims. High-profile cases are in heated debate over the definition of “received by” for the 20-day rule. And, of course, there is the question of what constitutes a “good” because services are not covered under these claims, and whether those goods have been sold in the ordinary course of business.

A member of the panel at CRF’s Fall Forum, Judge Christopher S. Sontchi, Chief Judge of The United States Bankruptcy Court for the District of Delaware, has presided over several cases determining “goods” and “receipt.” Notably, in one case, Judge Sontchi looked to the UCC definition of goods and subsequently held that electricity is not a “good” under 503(b)(9).

To be clear, a UCC filing is not without potential obstacles. Your UCC must be properly perfected and there is a narrow margin for error. But, ensuring a UCC has been properly perfected is less cumbersome than proving goods are goods, defining date of receipt and verifying goods are sold during ordinary course of business.

Rounding Out the Survey

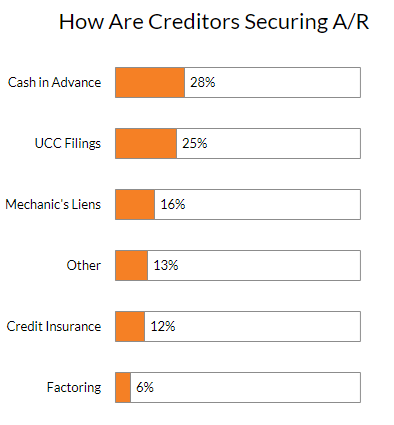

How Are Creditors Securing A/R?

For creditors securing their A/R the top two security measures were Cash in Advance and UCC filings.

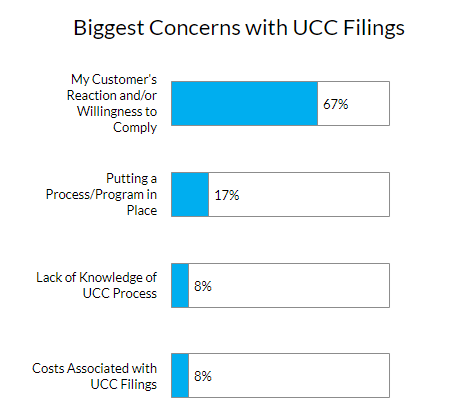

Biggest Concerns with UCC Filings

Despite concerns surrounding UCC filings, respondents certainly recognize the benefits of UCC filings. Benefits include being a secured creditor in a bankruptcy, the ability to repossess goods if customer defaults, the customer will consider creditor a greater payment priority and there would be public record of the debt.

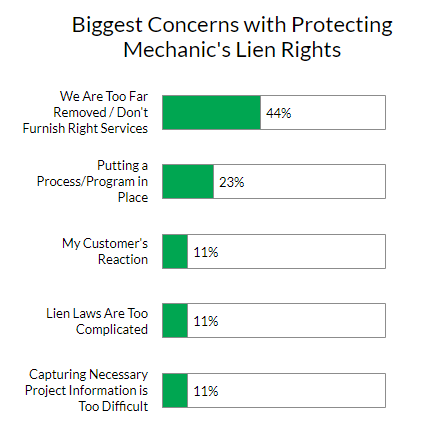

Biggest Concerns with Protecting Mechanic’s Lien Rights

Similar to what we see with UCC filings, respondents agree protecting mechanic’s lien rights would make them a secured creditor in the event of bankruptcy, customers would consider the creditor a greater payment priority and there would be public record of the debt.

Secured Transactions are Excellent Way to Secure A/R

Whether you file UCCs or mechanic’s liens:

- You are a priority. In bankruptcy, secured creditors have priority and are paid before unsecured creditors.

- You can sell more. Securing your A/R allows you to extend larger credit limits and sell to those accounts that were previously out of reach.

- Fewer write-offs. Fewer write-offs lower the costs associated with your product. Lower costs mean you can sell your product at a lower price while maintaining viable profit margins. Selling at a lower price makes your company more competitive, opening the doors to a larger market share. More sales with stable profit margins are a win.

- Improved DSO. Here’s a testimonial from one of our clients: “After implementing the lien/notice to owner program, we have seen our DSO numbers steadily decline each month, to an average of around 22 days. That is over a 30% improvement in our DSO since we first partnered with NCS.”

- Low cost solutions. UCC filings and preliminary notices/mechanic’s liens are truly a low-cost solution; especially when compared to the costs associated with chasing receivables.